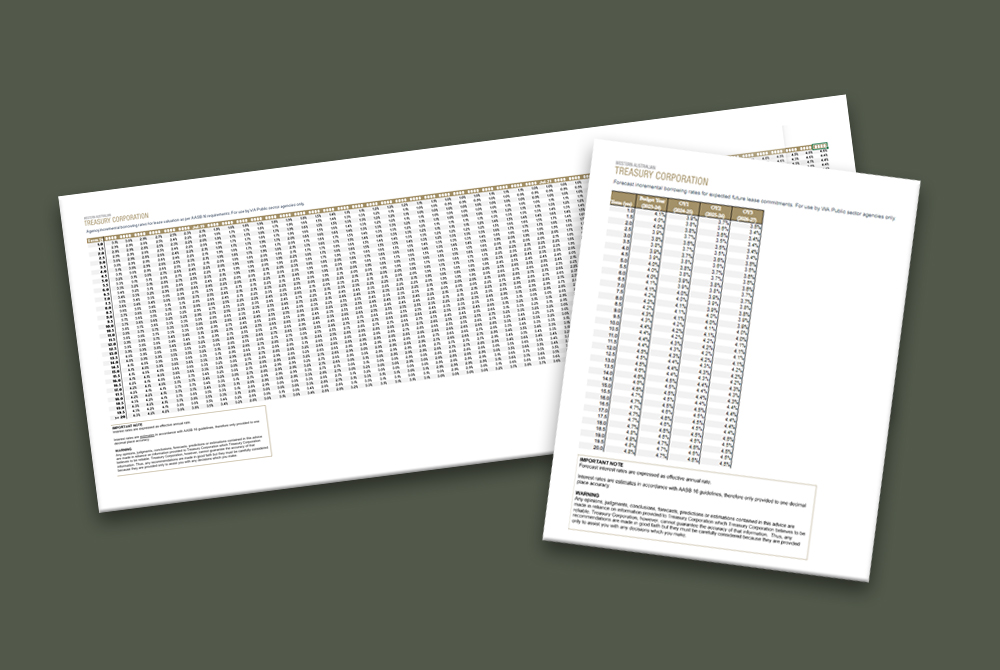

Actual rates for use in annual accounts

The database below provides incremental borrowing rates for use by Western Australian government entities, only as discount rates for determining the present value of lease payment obligations for which the implicit interest rate is unknown, in accordance with the requirements of AASB 16.

For leases commencing after inception, apply the rate for the month in which the lease commenced for the contracted term rounded to the nearest half year interval. This database is updated monthly, at the beginning of the month, by WATC.

For leases transitioning to AASB 16 on 1 Jan 2019 (for Calendar Year reporting) or 1 July 2019 (for Financial Year reporting), apply the rate listed for Jan 19 / Jul 19 for the remaining term of the lease rounded to the nearest half year.

- Borrowing Rates for Leases - July 2025

Forecast rates for future leases – for budgeting purposes only

The database provides forecast incremental borrowing rates for Western Australian government entities, to assist with estimating future lease liability for new (or replacement) leases, expected to be implemented within the budget out-years for the purpose of budget reporting only. It will be updated annually by WATC and is only available for a defined period.

The rate applicable can be applied for the (future) year within which a lease is expected to commence, for an expected contractual term rounded to the nearest half year interval.

Forecast rates for future leases must only be applied for budgeting purposes – when / if the actual lease commences, the actual rate from the above database must be applied.

AASB 16 Queries?

Contact Information

All queries on application of AASB 16 should be directed to the Department of Treasury at: Lease.StandardEnquiries@treasury.wa.gov.au

Issues with the above databases or the instructions for use can be made to WATC through: csoperations@watc.wa.gov.au

Banner images:

Top - WA Museum Boola Bardip, Perth. Image courtesy of Tourism Western Australia.

Below - Perth City. Image courtesy of Tourism Western Australia.